HMRC Mileage Rate Rises to 55p a Mile, Backdated to 6 April 2026

Quick answer

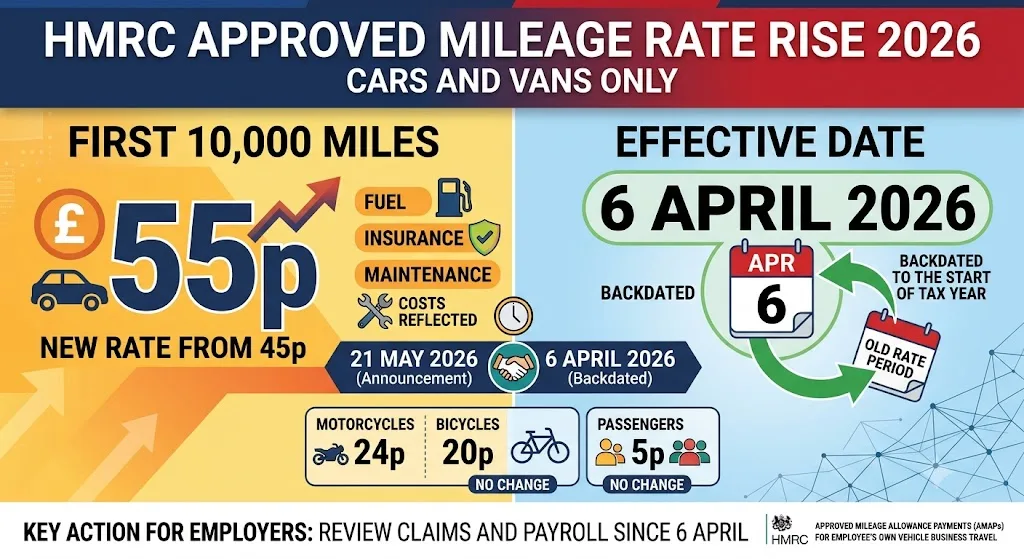

The approved mileage rate for cars and vans rises from 45p to 55p per mile for the first 10,000 business miles, the first increase in 15 years. It applies for the whole 2026/27 tax year, so miles driven since 6 April already qualify.

The first mileage rate rise in 15 years

The headline HMRC mileage rate for cars and vans is rising from 45p to 55p per mile for the first 10,000 business miles in the tax year. The government announced the increase on 21 May 2026, and the legislation to deliver it sits in the Taxation (Energy and Vehicles) Bill, presented to Parliament on 24 June 2026. Crucially, the change is backdated to 6 April 2026, so every business mile you have driven since the start of this tax year already counts at the new rate.

This is the first change to the Approved Mileage Allowance Payment (AMAP) rate since 2011/12. Fifteen years of frozen rates meant drivers were absorbing rising fuel, insurance and servicing costs on a 2011 allowance. A 10p rise does not fix all of that, but for a typical 8,000-mile-a-year driver it is worth £800 more tax-free allowance every year.

Old vs new rates

| Vehicle | Rate to 2025/26 | Rate from 2026/27 | Change |

|---|---|---|---|

| Car or van, first 10,000 miles | 45p per mile | 55p per mile | +10p |

| Car or van, above 10,000 miles | 25p per mile | 25p per mile | No change |

| Motorcycle | 24p per mile | 24p per mile | No change |

| Bicycle | 20p per mile | 20p per mile | No change |

| Passenger rate (per colleague) | 5p per mile | 5p per mile | No change |

The same 55p figure also flows through to the simplified expenses flat rate that self-employed people use for vehicle costs, because the Bill amends both the employee rules (section 230 of ITEPA 2003) and the trading rules (section 94F of ITTOIA 2005). Electric and hybrid cars use the same rates as petrol and diesel.

Example 1: employee whose company pays the old rate

Marcus does 8,000 business miles a year in his own car and his employer reimburses him at 45p per mile. Here is his position for 2026/27:

| Line | Amount |

|---|---|

| Employer pays 8,000 miles at 45p | £3,600 |

| HMRC approved amount: 8,000 miles at 55p | £4,400 |

| Shortfall he can claim Mileage Allowance Relief on | £800 |

| Tax back at basic rate (20%) | £160 |

| Tax back at higher rate (40%) | £320 |

His employer does not have to raise its rate to 55p, but until it does, Marcus should claim the relief himself through Self Assessment or a P87 claim. Our Mileage Allowance Calculator works this shortfall out for you, and the Mileage Tracker keeps the log HMRC expects to see.

Example 2: self-employed driver on simplified expenses

Priya is a self-employed courier who drove 12,000 business miles this year and uses the flat-rate mileage method instead of actual vehicle costs:

| Calculation | Old rules | New rules |

|---|---|---|

| First 10,000 miles | 10,000 x 45p = £4,500 | 10,000 x 55p = £5,500 |

| Next 2,000 miles | 2,000 x 25p = £500 | 2,000 x 25p = £500 |

| Total deduction | £5,000 | £6,000 |

That extra £1,000 deduction cuts her taxable profit. As a basic-rate taxpayer she saves 20% income tax plus 6% Class 4 National Insurance, so the rise is worth about £260 a year to her. Check your own numbers with the Self-Employed Tax Calculator.

Example 3: employer already paying more than 45p

Some employers pay 50p or 55p per mile and, until now, anything above 45p was taxable as extra pay. From 2026/27 an employer can pay up to 55p per mile for the first 10,000 miles with no tax or National Insurance at all. An employee doing 6,000 miles at 55p receives £3,300 entirely tax-free; under the old rules £600 of that would have been taxed through the payroll.

What else is in the Taxation (Energy and Vehicles) Bill

- Electricity Generator Levy rises from 45% to 55% on exceptional receipts from 1 July 2026.

- Vehicle Excise Duty holiday for HGVs: a temporary 12-month VED exemption for certain heavy goods vehicles applies from 1 July 2026 to 30 June 2027.

- What is not in it: the pay-per-mile charge for electric vehicles (eVED) announced at the 2025 Budget. That is still planned for April 2028 at 3p per mile for EVs and 1.5p for plug-in hybrids, but it will need its own legislation. You can estimate the future cost with our EV Pay-Per-Mile Tax Calculator.

Common mistakes to avoid

- Forgetting the backdating. Miles driven since 6 April 2026 qualify at 55p even though they happened before the announcement. Do not claim them at 45p.

- Applying 55p above 10,000 miles. The over-10,000 rate stays at 25p.

- Claiming without records. HMRC expects a mileage log with dates, journeys and business purpose. A diary entry per trip is enough; reconstructed guesses are not.

- Missing the passenger rate. Carrying a colleague on a business journey still adds a tax-free 5p per mile on top.

Your action checklist

- Start logging business miles now if you are not already; the Mileage Tracker makes it painless.

- Employees: check what rate your employer pays and claim relief on any gap below 55p.

- Self-employed: use 55p for the first 10,000 miles of 2026/27 when you file, and compare the flat rate against actual costs with the Expenses Checker.

- Employers: decide whether to raise reimbursement rates to the new tax-free maximum and update your expenses policy.

Sources

Written by

Laura Michelle Davis — Chartered Tax Adviser (CTA)

ACCA · CTA (Chartered Tax Adviser) · ATT · BSc Economics, UC Berkeley

Laura Michelle Davis is a Chartered Tax Adviser (CTA) who also holds the ACCA and ATT qualifications and a BSc in Economics from UC Berkeley. She specialises in UK personal tax, covering income tax, National Insurance, self-employment and capital gains, and has built her career making complicated rules easy to follow. At TaxFly, Laura writes and edits the tax guides and explainers, checking that figures reflect current HMRC rates and that every explanation answers the question a real person is actually asking. Her goal is plain-English clarity you can trust and act on.