Payrolling Benefits in Kind: What Changes from April 2027

Quick answer

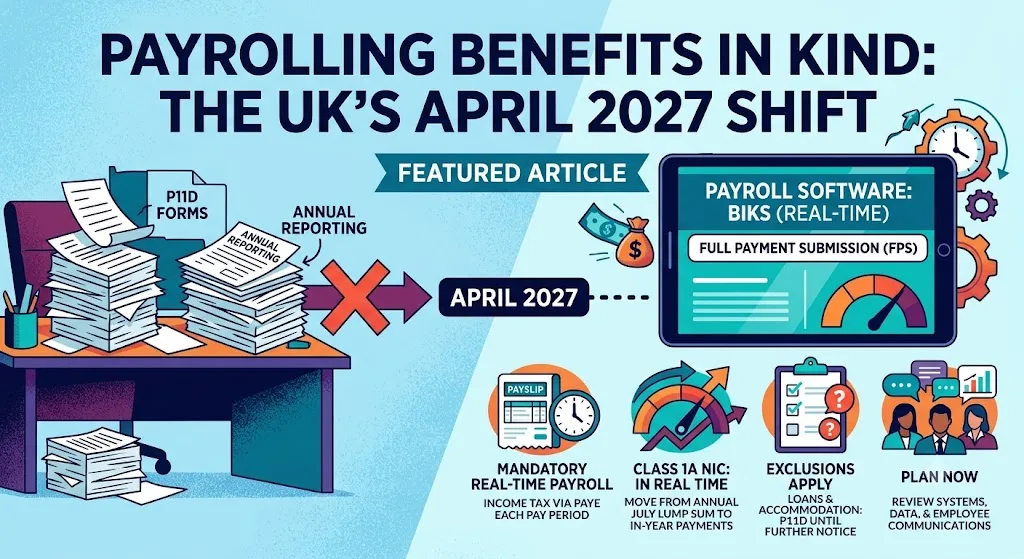

HMRC has confirmed that company cars, fuel and medical benefits must be taxed through payroll from 6 April 2027, with most other benefits following in 2028. Here is the full timetable, what P11Ds survive, and what employers and employees should do now.

Quick answer

From 6 April 2027, employers must report and tax company cars, car fuel, vans, van fuel and employer-provided medical benefits through the payroll in real time, instead of on an annual P11D. Most other benefits in kind follow from April 2028. Employment-related loans and living accommodation stay outside the mandatory rules and can still be payrolled voluntarily or reported on a P11D. HMRC confirmed this two-phase timetable on 15 June 2026, after delaying the original April 2026 start date.

Key facts at a glance

| Question | Answer |

|---|---|

| What is changing | Benefits in kind move from annual P11D reporting into real-time payroll (the Full Payment Submission) |

| Phase 1 start | 6 April 2027: company cars, car fuel, vans, van fuel, medical benefits |

| Phase 2 start | April 2028: most remaining benefits in kind |

| Always excluded from mandation | Employment-related loans and living accommodation (voluntary payrolling allowed) |

| Last normal P11D year | 2026/27, filed by 6 July 2027 |

| Who announced it | HMRC, 15 June 2026 (originally planned for April 2026) |

What payrolling a benefit actually means

Today, most benefits in kind are reported once a year on form P11D. HMRC then adjusts the employee's tax code so the tax trickles in during the following year, always one step behind reality. Payrolling replaces that loop: the cash value of the benefit is divided across the year's pay periods and added to taxable pay each payday, so the tax is collected in the same year the benefit is enjoyed.

Here is how the process changes for a payrolled benefit:

- The employer works out the cash equivalent of the benefit for the year, exactly as now.

- That value is split across the number of paydays (12 for monthly payroll).

- Each payday, the slice is added to taxable pay for PAYE purposes only. The employee does not receive extra money; they just pay tax on the benefit as they go.

- The benefit is reported to HMRC on the Full Payment Submission (FPS), the same real-time report employers already send every payday.

- No P11D is needed for that benefit, and no tax-code adjustment chases the employee into the following year.

The timetable in full

| Tax year | What applies |

|---|---|

| 2026/27 (now) | Current rules. P11Ds due by 6 July 2027. Voluntary payrolling available if you registered with HMRC before 6 April 2026. |

| 2027/28 | Phase 1 mandatory: company cars, car fuel, vans, van fuel and medical benefits must go through payroll. Other benefits stay on P11D (or voluntary payrolling). |

| 2028/29 | Phase 2: most remaining benefits in kind become mandatory through payroll. P11Ds survive only for loans and accommodation where these are not voluntarily payrolled. |

Example 1: the company car driver

Amira has a company car with a cash equivalent of £6,000 a year and pays higher-rate tax at 40%, so the car costs her £2,400 in tax annually.

| Now (P11D and tax code) | From April 2027 (payrolled) | |

|---|---|---|

| How the £6,000 is reported | P11D after year end | £500 added to taxable pay each month via FPS |

| How the £2,400 tax is collected | Tax code reduced the following year | £200 extra PAYE each month, in real time |

| Risk of surprise bills | Yes, when the code lags a car change | Minimal: tax tracks the benefit month by month |

Her payslip's taxable gross rises by £500 a month but her cash pay does not change; only the tax deduction does. Check what a car costs you with our Company Car Tax Calculator.

Example 2: the employer with private medical cover

A design agency provides private medical insurance costing £1,200 a year to each of its 15 staff. From April 2027 the agency must put £100 a month per employee through payroll as a taxable benefit instead of filing 15 P11Ds the following July. Employer Class 1A National Insurance at 15% still applies, costing £180 per employee per year, and moves to real-time reporting alongside the benefit. The agency saves the July P11D scramble, but its payroll software and processes must be ready before the first April 2027 payday. Our P11D Generator stays useful for the 2026/27 filings and, after that, for loans and accommodation.

What employers should do before April 2027

- Audit your benefits now. List every benefit you provide and tag which phase it falls into.

- Ask your payroll software provider when payrolling and real-time Class 1A support will be ready.

- Consider voluntary payrolling early. Registering ahead of a tax year lets you move before you are forced to, one benefit type at a time.

- Budget for the cash-flow shift on Class 1A, which moves from an annual payment to real time for payrolled benefits.

- Tell your employees what is coming. Their payslips will show higher taxable pay and their tax codes will be rebuilt to remove benefit deductions; without warning, that reads as a pay cut.

What it means for employees

You will not pay more tax overall; you will pay the same tax sooner and more accurately. The main transition risk is 2027/28 itself: if your tax code still carries a benefit deduction while your employer starts payrolling the same benefit, you would briefly pay tax twice. HMRC and employers are expected to strip benefit adjustments out of codes as payrolling starts, but it is worth checking your own. Our tax code guides explain every letter and number, and the Income Tax Calculator shows what your take-home should look like.

Common mistakes to avoid

- Treating April 2027 as a soft deadline. Phase 1 is mandatory. If you run payroll for anyone with a company car, van or medical cover, your first 2027/28 payday must handle it.

- Forgetting 2026/27 P11Ds. The old regime runs fully until 6 July 2027. Payrolling from April 2027 does not cancel the P11Ds due for the year before.

- Assuming everything is phase 1. Gym memberships, professional subscriptions and most other benefits stay on the old rules until April 2028.

- Employees ignoring their tax code in 2027. Check that benefit deductions disappear from your code once your employer starts payrolling.

Sources

Written by

Laura Michelle Davis — Chartered Tax Adviser (CTA)

ACCA · CTA (Chartered Tax Adviser) · ATT · BSc Economics, UC Berkeley

Laura Michelle Davis is a Chartered Tax Adviser (CTA) who also holds the ACCA and ATT qualifications and a BSc in Economics from UC Berkeley. She specialises in UK personal tax, covering income tax, National Insurance, self-employment and capital gains, and has built her career making complicated rules easy to follow. At TaxFly, Laura writes and edits the tax guides and explainers, checking that figures reflect current HMRC rates and that every explanation answers the question a real person is actually asking. Her goal is plain-English clarity you can trust and act on.